Arva AI’s blog

Discover industry insights, deep dives, product updates, and more.

Search...

Search...

Search...

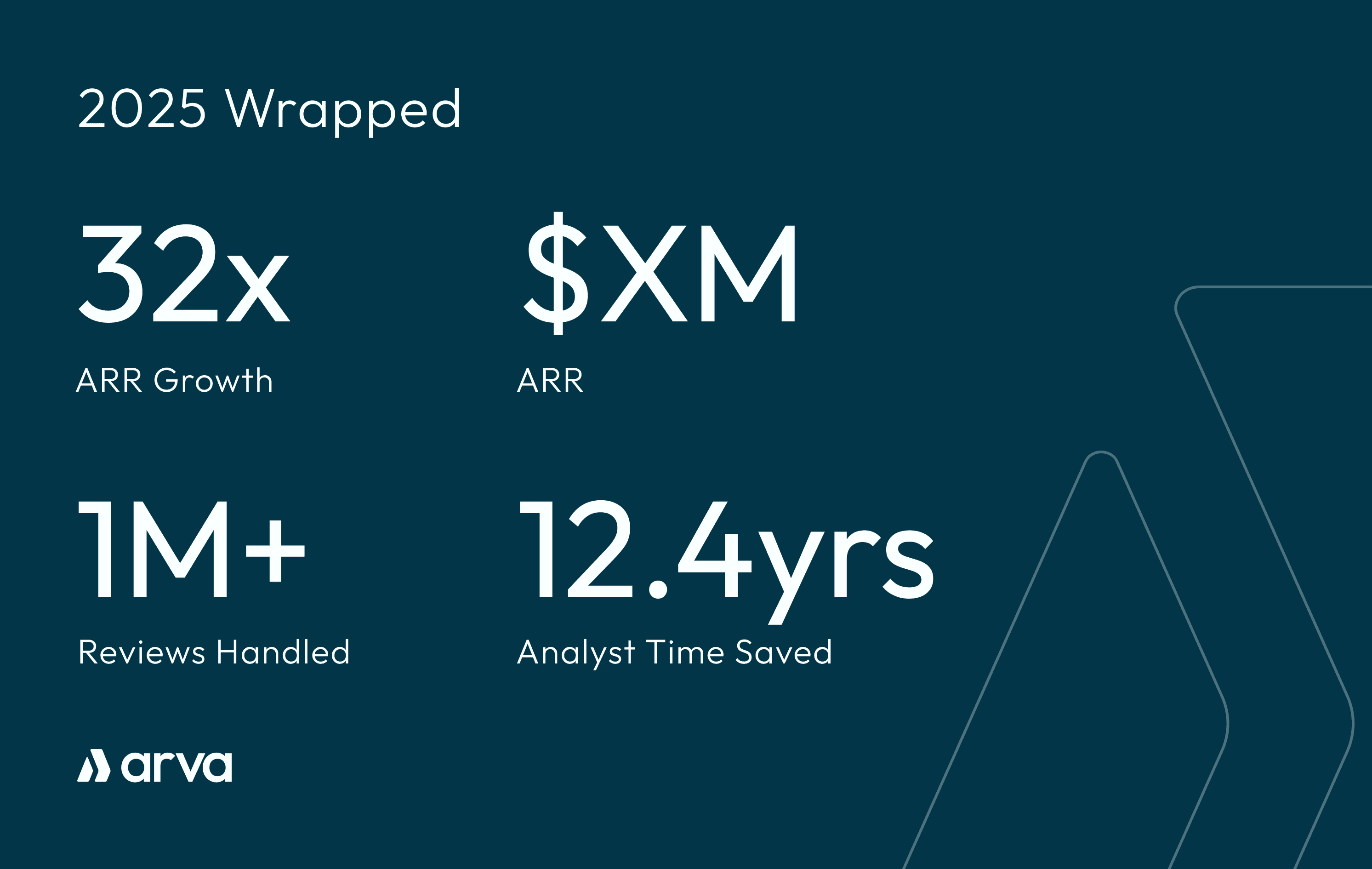

Automate 92% of your financial crime reviews with Arva AI

Power your AML financial crime compliance with an enterprise AI workforce

Automate 92% of your financial crime reviews with Arva AI

Power your AML financial crime compliance with an enterprise AI workforce

Automate 92% of your financial crime reviews with Arva AI

Power your AML financial crime compliance with an enterprise AI workforce

Arva AI is a platform to build, deploy, & monitor your AI workforce, automating 92% of all financial crime reviews

Product

Arva AI is a platform to build, deploy, & monitor your AI workforce, automating 92% of all financial crime reviews

Product

Arva AI is a platform to build, deploy, & monitor your AI workforce, automating 92% of all financial crime reviews

Product